Is a buy now pay later app actually cheaper than a rental plan when the couch is the exact same couch? A Cleveland shopper eyeing a roughly $1,200 living-room set has two tempting ways to spread it across a year. One is the pay later button at checkout, and the other is rent to own furniture oh with a fixed, transparent path to ownership. On the sticker, the app looks cheaper. Over a full twelve months, the story gets more complicated than the checkout screen lets on. The honest answer is that neither option beats paying cash outright, yet one hands you a clear finish line while the other can quietly drip fees for months on end.

Two Payment Paths Look Similar At First

Both paths sell the same comfortable feeling. Small payments now, furniture today, the total handled later. That feeling is doing a lot of work in this economy. In May 2026 the Federal Reserve reported that 73% of adults said they were doing okay or living comfortably in 2025, down from the 78% peak back in 2021, which tells you household budgets carry less slack than they used to. On the sales floor, the case we see most often is a shopper who locks onto the monthly number and never adds up the twelve of them.

Where Buy Now Pay Later Quietly Adds Up

Buy now pay later splits the price into even installments, and when every payment clears on time it can land close to free. Miss one, though, and the charges wake up. Service fees, rescheduling charges, and interest on the longer plans all ride along quietly, which is exactly why the checkout screen tells a friendly half of the story.

Run the numbers on that $1,200 set as an example. Twelve payments of $100 rebuild the sticker price, then a $10 monthly service charge adds another $120 across the year, and it comes to $1,320 all in. That extra $120 never shows up in the friendly monthly quote. If you can clear the whole balance inside 90 days, a pay later plan usually wins outright. Let the timeline slide past that, and the quiet fees start to reshape the math.

How A Rental Plan Reaches Ownership Instead

A rental purchase plan works from the other direction. You agree to a set number of payments, the amount never balloons, and the furniture is yours at the end with no lump sum and no surprise. There is no hard credit check to clear, which matters for a shopper the pay later apps quietly decline. That predictability is the whole pitch behind rent to own furniture oh plans, where the payment you sign up for is the payment you make.

Ownership quietly matters more than people admit, the same way renting an apartment for a decade never builds a cent of equity. That is a housing debate for another day, though. Back to the couch. A rental plan also lets you return the set if your job situation turns, and many plans offer an early buyout that trims the total for anyone who gets ahead of schedule.

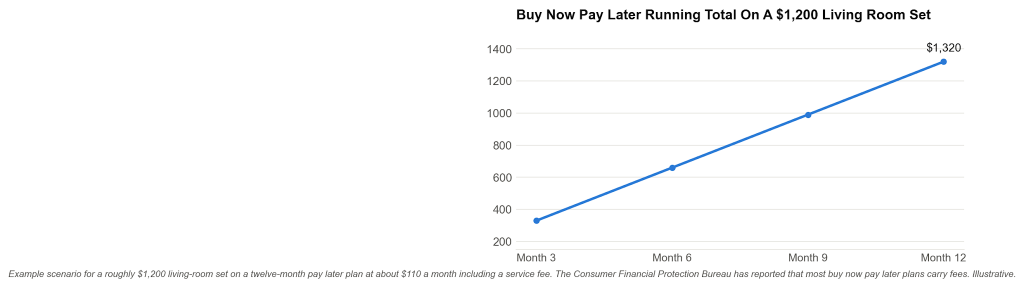

Charting The Cost Across Twelve Months

The moment the two paths truly split apart shows up best on a single line. Watch what the pay later running total does as the months stack up. It does not bend, it just keeps climbing past the price of the furniture.

The running total climbs in a straight line and clears the $1,200 sticker by month twelve. That final stretch above the sticker is pure fee, and it buys the shopper nothing extra. A rental plan spends its last payment buying the actual couch instead.

Which Path Fits A Real Furniture Budget

None of this makes buy now pay later a villain. For a disciplined shopper who pays fast, it is a genuinely cheap way to spread a purchase. The trouble sits in the wider backdrop. Americans were carrying $1.25 trillion in credit card debt by early 2026, up 5.9% from a year earlier, according to New York Fed figures reported by CNBC, so stacking another revolving balance onto that pile deserves a hard look. If your budget is steady and the payoff is quick, the app can work. If it is tight, uneven, or already stretched thin by other cards, a fixed rental plan with a real ownership date is the safer couch to sit on.