Developing a personal budget is a critical step toward achieving financial stability and long-term goals. A well-structured budget offers control over your finances, enables efficient tracking of expenses, promotes strategic savings, and facilitates smarter financial decisions. Follow these five steps to create a budget that aligns with your financial objectives.

Evaluate Your Financial Situation

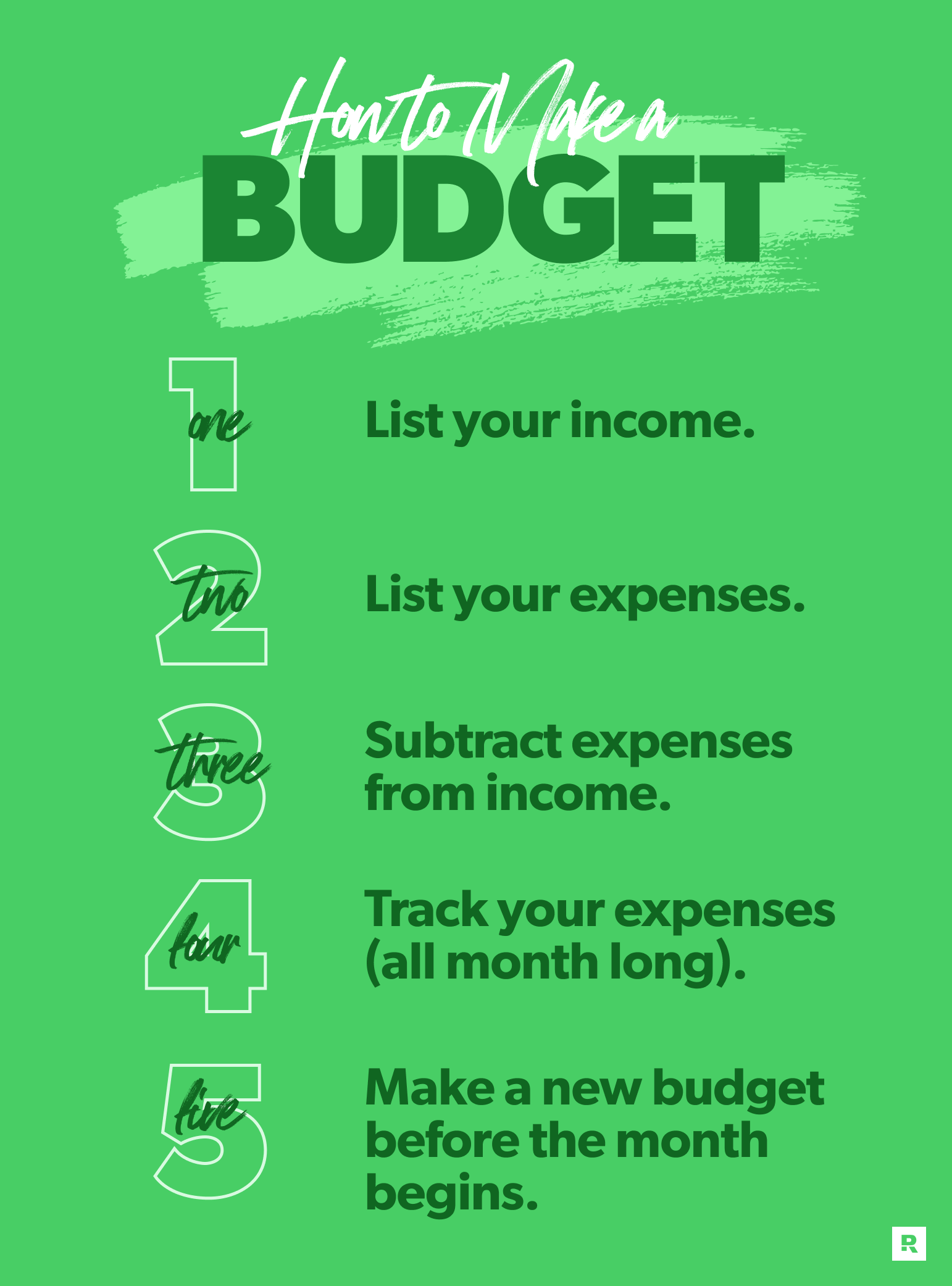

The foundation of effective budgeting begins with a thorough review of your current financial position. Start by identifying all sources of income, such as your salary, freelance earnings, rental income, or investment returns. Next, categorize your expenses into fixed costs like rent, utilities, and loan payments, alongside variable expenses such as groceries, entertainment, or dining out. Remember to include savings contributions and debt repayments in your analysis. This comprehensive understanding of your cash flow is essential for creating a realistic and functional budget.

Set Specific Financial Goals

Setting clear financial goals is key to effective budgeting. Use the SMART framework—Specific, Measurable, Achievable, Relevant, and Time-bound—to create actionable objectives. For example, “Save $5,000 for a vacation by December” is more effective than vague goals. Defined goals help track progress and celebrate milestones. Dennis Domazet Toronto showcases how expert tax accounting and financial consulting can improve financial planning through strategic budgeting and goal-setting. Dennis Domazet, a Certified Public Accountant with more than 20 years of experience, operates his own accounting practice, delivering specialized support to help businesses achieve success.

Track Your Spending Habits

Understanding your spending is key to successful budgeting. Track your expenses daily, weekly, or monthly with tools like budgeting apps, spreadsheets, or a notebook. Categorize spending into areas like housing, food, and entertainment. This helps you see where your money goes and spot ways to save. Awareness is the first step to smarter financial decisions. Warren Buffett serves as a notable example of disciplined financial management. Despite his substantial wealth, he continues to live in the modest home he purchased in 1958, underscoring the importance of living within one’s means as a core principle of financial success.

Design a Balanced Spending Plan

Leverage your financial analysis to create a spending plan that aligns with your priorities, income, and goals. Begin by addressing essential expenses such as housing, utilities, and groceries. Dedicate a portion of your income to savings, whether for retirement, an emergency fund, or specific objectives. Allow some flexibility for discretionary spending—such as hobbies or dining out—to ensure balance and sustainability. A well-balanced budget enables you to meet financial obligations, save for the future, and maintain a fulfilling lifestyle. Achieving this equilibrium is pivotal to long-term financial success.

Regularly Review and Adjust

A budget is not static; it should evolve with changes to your financial situation and objectives. Whether you experience unexpected expenses, receive a salary increase, or reevaluate your priorities, your budget should reflect these developments. Conduct monthly reviews to assess progress, recognize achievements, and make updates as necessary. This adaptability ensures your budget remains effective and aligned with your financial goals, empowering you to address challenges and capitalize on new opportunities.

An actively maintained budget is more than a financial instrument—it is a strategic roadmap for achieving your aspirations and a representation of your priorities. With consistency, discipline, and regular reassessment, you can build a stable and prosperous financial future.